If you’re a business owner who doesn’t know the VAT codes lists, you’ll require assistance. It would be challenging to charge VAT to your customers and pay it to the HMRC if you didn’t understand anything about it.

According to research, 19% of small business owners are concerned that they have missed something on their VAT return, while 18% are worried they have made a mistake.

Therefore, having a thorough understanding of how VAT tax codes function (and how VAT works in general) will aid in accurate record-keeping and the avoidance of VAT-related errors.

Table of Content

What are VAT codes?

Before we get into the VAT tax codes, we must first understand what they are.

HMRC created VAT codes to help people figure out how much VAT they should pay on products and services. These codes are alphanumeric and include the VAT rate as well as alphabets.

It’s important to note that the VAT code differs between the sales and purchase forms. Once you’ve registered for VAT, you must collect VAT on all vatable supplies and deposit the same with the HMRC regularly.

If you purchased a product for your business from a VAT-registered business, you can claim the input tax and pay the difference to HMRC.

You can easily understand this concept thanks to a simple formula.

Output VAT = paid by the customer.

Input VAT = paid to the supplier.

HMRC’s standard VAT rate is 20%, but it varies depending on the type of business and goods or services provided.

If you sell necessary commodities like food or children’s clothing, you won’t be charged VAT, which is known as Zero-rated.

Tax exemption differs from zero-rating in that you do not charge VAT to your consumers in both cases. However, the VAT rate on household electricity and children’s toys is lower (5%).

You must provide multiple UK VAT codes based on the goods and services when completing VAT returns. If you enter the wrong VAT code, you may pay the incorrect amount. HMRC will charge a penalty if you pay less than the required amount.

Commonly used UK VAT codes

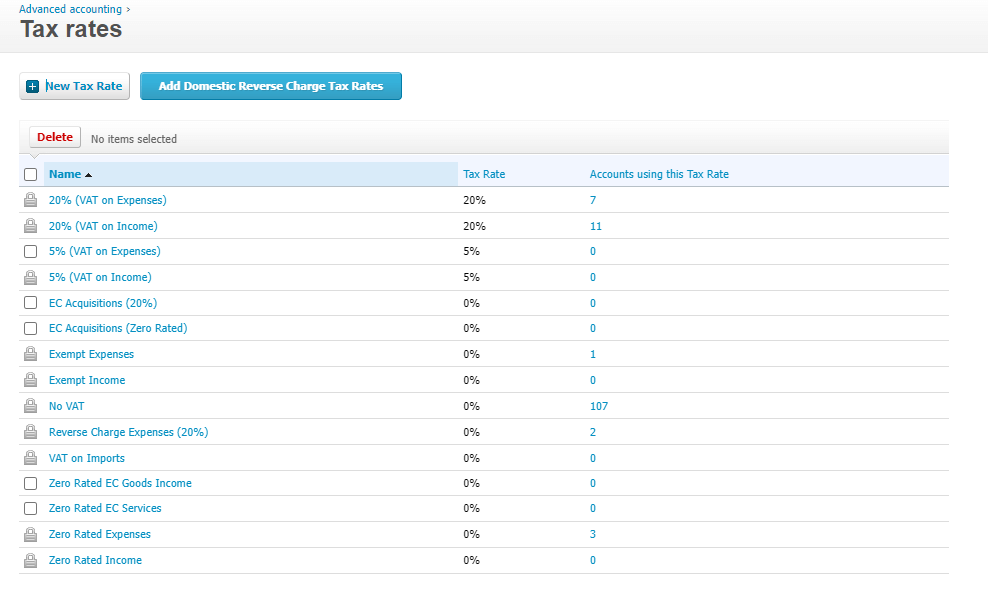

You will see a list of several VAT codes in yoru accounting software when you file your VAT return digitally, depending on the sorts of goods and services your business offers.

Following is a screenshot from Xero showing various tax rates.

Your business may be qualified to pay a lower VAT rate or be excluded totally in specific circumstances. Therefore, it’s advisable to study all of the VAT details thoroughly. Before selecting a VAT code other than 20%, visit the GOV.UK website ensures you’re selecting the correct code.

Keep in mind that if you’ve chosen the Flat Rate Scheme, your VAT codes won’t always appear the same because the amount of VAT you pay to HMRC will differ based on your sector.

Commonly used EC VAT codes

Suppose your company is VAT-registered and you buy goods or services from another VAT-registered company in another EC Member State. In that case, you should not be charged VAT since you give the supplier your VAT registration number.

The supplier will then be responsible for using the reverse charge procedure to render this charge nil.

The burden for documenting the VAT transaction for that specific commodity or service is shifted from the vendor to the buyer with a VAT reverse charge.

It eliminates the need for merchants to register in the country where their goods are produced. If the supplier is charged VAT on costs related to services or the delivery of goods under the reverse charge, they can reclaim it through an EU VAT reclaim.

If you’re the supplier and shipping goods to clients in an EC Member State, you shouldn’t charge VAT if they provide you with a valid VAT registration number. You can look up the VAT registration number here.

By ‘charging’ your consumer utilising the reverse charge technique, you would be the one to make the VAT nil. To comply with regulatory requirements, the VAT invoice you issue in this case must include the words reverse charge.

If you didn’t receive a valid VAT number, use the appropriate VAT rate.

For example, use one of the below EC VAT rates for transactions that qualify.

| VAT Code | Description | Code used on sales form | Code used on purchase form |

| 20.0%ECG | B2B purchases of goods within the EU. The customer must pay any VAT payable in business to business transactions via the reverse charge procedure. The consumer must behave as though they are both the seller and the receiver of goods. | N/A | +/ VAT at 20% to Box 2 and 4+/- Net Purchase to Box 7 and 9 |

| 20.0% ECS | Intra B2B of services. The customer must use the reverse charge procedure to account for any VAT due in business-to-business transactions. The consumer must act as both the provider and the receiver of services. | N/A | +/- VAT at 20% to Box 1 & 4+/- Net Purchase to Box 6 & 7 |

| 0.0% ECS | B2B service supply throughout the EU. Used for intra-EU service sales between businesses. The applicable UK VAT rate is charged if the EU customer is not VAT registered. It’s critical to keep track of the location of supplies for services. – In B2B, the place of supply is the location of the service receiver. The site of supply for B2C (business to consumer) is the provider’s location. | Net Sale to Box 6 | +/- VAT at 0% to Box 1 & 4 +/- Purchase to Box 6 & 7 |

| 0.0% RC | Reverse Charge within the EU. Used for B2B transactions within the EU using mobile phones and computer chips. | Net Sale to Box 6 | N/A |

How to keep VAT records?

VAT registration is required in the UK if a company’s yearly vatable supplies exceed £85,000.

VAT registration is unnecessary for businesses with less than this threashold; hence these codes are not required. However, in practice, many businesses voluntarily register for VAT, in which case the entire VAT law applies.

Let’s discuss how to retain these VAT records now that you know the VAT codes in the UK.

Businesses must keep VAT records for a minimum of six years.

However, if you use VAT MOSS services, you must keep them for ten years.

With the recent digitisation of taxation, it is necessary to retain all VAT data digitally. To guarantee that all VAT records are valid, you must utilise MTD compliant bookkeeping software.

If you misplace your VAT invoice, contact the supplier and request a duplicate.

Businesses must keep the following records:

- All copies of your invoices and bills

- Notes of debit and credit

- Agreements for self-billing (Customers prepare the invoice in this aspect)

- Self-billing suppliers’ names, addresses, and VAT numbers

- Documentation of all of your imports and exports

- Keep track of the zero-rated, VAT-exempt stuff you buy or sell.

- Bank statements, check stubs, cash books, till rolls, and paying in slips are all examples of documents.

Businesses that are required to preserve digital records under Making Tax Digital should keep the following information:

Modes:

- Name of company, VAT registration, and mailing address

- It is charged on all purchases of goods and services. Everything you brought rented or leased.

- Accounting schemes for VAT that you use

- Any changes you’ve made to a return

- Time and value of supply (not including VAT) for items purchased or sold

- The VAT rate applied to products and services you supply

- A retail scheme’s daily gross takings

- Items for which you can reclaim VAT in a flat-rate plan.

Apart from this, it’s a good idea to keep track of any charitable contributions your company has made, as well as any third-party business or employee expenses that fall under petty cash.

Wrapping up

When filing your VAT returns, it’s hard to overlook VAT codes if your company is VAT registered.

Understanding which VAT codes apply to each of your company’s products and services will help you pay the correct amount of VAT, avoid penalties, and keep your company’s finances in order.

It can be challenging to understand VAT codes and the laws that go along with them. If you need more information, try employing an online accountant to assist you in following the rules and paying the proper VAT amount.