Anyone can start a business; you don’t need a renowned degree or a large sum of money to start.

However, you will need a basic set of actions to give yourself a realistic time range and a clear goal to strive forward.

We’ve got tips on everything from developing a business strategy in the UK and legal frameworks.

While it may seem overwhelming, you could join one of the six million SMEs in the United Kingdom with dedication and passion.

Continue Reading our guide to learn how to open a new business in the UK.

Table of Content

What do you need to start your own company?

You’ll need the following in addition to a brilliant idea that you’re passionate about:

Training and courses: Depending on your industry, you might require specialised training or choose a standard business qualification.

Licence: If you want to sell food, play music, or trade on the street, check the government website to determine if you need a business licence.

Specialised tools: Make sure you account for any necessary equipment or devices in your budget.

Products: You’ll need to gather your stock, open a shop or sell your products.

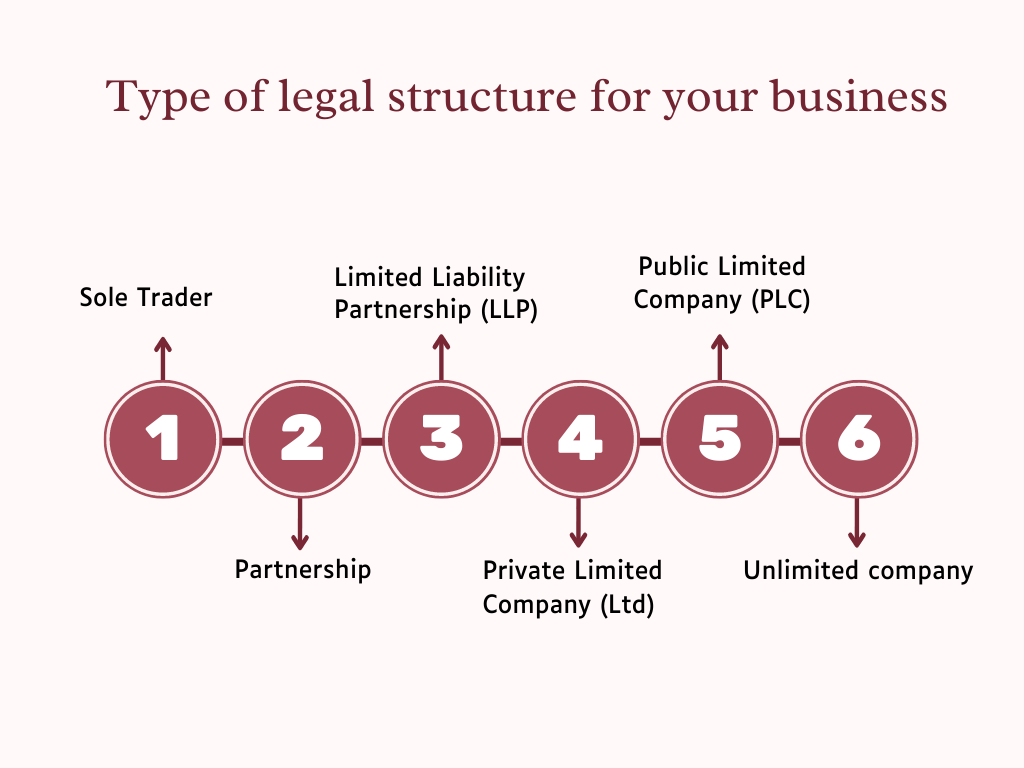

Choosing the legal structure for your business

1. Sole Trader

The business is owned and run by one individual. Between the owner and the industry, there is no legal separation. The sole trader keeps all of the gains but also all of the company’s liabilities.

2. Partnership

It is the easiest alternative when more than one business owner and two or more people share the costs, risks, and responsibilities. There are no requirements for equal shares, and each person’s liability is proportional to their part.

The drawback is that, as a single trader, partners are not financially protected. If the company fails, you may be held accountable for your partner’s portion of the debt.

3. Limited Liability Partnership (LLP)

This hybrid form combines the benefits of a partnership and a limited liability company.

A limited liability partnership (LLP) is a separate legal entity. It is controlled by the Companies Act and is registered at Companies House.

The personal liability of members is limited.

An LLP has no shareholders or directors and is taxed similarly to a partnership, which pays tax on its share at a rate appropriate to its circumstances.

4. Private Limited Company (Ltd)

This type of business is a legal entity independent of the people who operate it. Limited corporations must have at least one director and one shareholder and must be registered with Companies House. The company’s stock cannot be traded publicly.

5. Public Limited Company (PLC)

PLCs are differentiated from limited companies because their stock can be traded publicly. A minimum share capital of £50,000 is required, with at least 25% paid before start-up.

6. Unlimited company

This business structure isn’t prevalent in the United Kingdom.

It entails shareholders having shared unlimited liability for business debts, which means they can be compensated with personal assets if the firm investments fail to cover expenses.

How to start a business in the UK

1. Write a business plan

UK entrepreneurs need a business plan. It will assist you in determining whether or not your business ideas are likely to thrive and be long-term sustainable.

You’ll need to do market research and budget estimates. The business plan and cash flow prediction templates are available from the UK government website.

2. Secure funding and finance

What is the minimum sum of capital required to start a business? It will differ based on the nature of your goods or service. You may not need much initial investment if you’re starting small.

However, if you’ve identified several charges in your budget, you’ll need to figure out how to pay for them. Will you make use of your savings? Or will you seek assistance in beginning a new business (such as loans from friends, family, or a bank)?

Keep in mind that grants for new enterprises may be available to help with the financial burden. The advantage of a small business grant over a loan is that you usually don’t have to pay it back.

It’s a good idea to look into government support for new enterprises.

The Start-Up Loan, offered by the British Business Bank, is another government-backed initiative. At a fixed interest rate of 6% per year, you can borrow up to £25,000. You’ll also get a free year of mentoring.

3. Decide on your structure

As previously stated, you should select the business structure that best represents your company.

4. Choose a business name and address

You’re free to use your name if you’re a sole trader. When registering your UK business for tax purposes and entering the company register, you’ll need an address.

Only a few companies are required to register their name, but others can do so as a trademark to prevent others from trading under the same name.

You must appoint directors and a company secretary, calculate your shares and shareholders, write your memorandum and articles of organisation, open a separate bank account, and register for corporation tax if you’re forming a limited business.

5. Buy your new business insurance

The nature of your company determines the type of business insurance you’ll require.

You can customise your policy to protect yourself against the costs of everyday risks like accidents, damage, and legal fees, whether you run an online store or provide a service. You can also add specific covers if you need to safeguard stock or tools.

You can choose from a variety of covers, including:

- public liability insurance – this is essential if clients visit your premises or you carry out work on customer sites

- professional indemnity insurance – protects you if a customer loses money because you provide careless advice, designs or services

- employers’ liability insurance – this is a legal necessity if you have employees

- legal expenses insurance – covers company legal expenses or prosecution fees

- Business health insurance – affordable healthcare cover for you and your employees

6. Register with HM Revenue and Customs

Understanding the legal and accounting duties of owning a corporation is critical.

There is a £1,000 tax-free allowance, but you must register with HMRC afterwards.

For tax purposes, you must register your UK business with HMRC. Limited companies must register with Companies House for £12 (online) or £40 (offline) (by mail).

Legislation that may affect your business

Legislations are laws and regulations that must be followed when operating a business.

1. Employment law

Employees’ rights, as well as their health and safety, are protected by employment legislation. Below we will discuss the primary laws to consider for those employing staff.

2. Health and Safety at Work Act of 1974

The premises or machinery must not harm workers’ health. If you have five or more employees, you must have a written health and safety policy and risk assessments that must be documented and communicated to the workers.

3. Equal Pay Act of 1970

Employees must be compensated equally regardless of gender for work of equal worth.

4. Race Relations Act of 1976

Discriminating against someone because of their skin colour, race, or ethnic group is illegal.

5. Employment Protection Act of 1978

Employers are required to provide employees with a formal employment contract. It protects workers from unfair dismissal and offers them the right to redundancy pay if their position is no longer needed after two years.

6. Consumer Protection

Consumer protection rights protect customers from unfair company practices.

7. Sale and Supply of Goods Act

Goods must be of a decent standard. It applies to any products that consumers have recognised and decided to purchase.

8. Trade Descriptions Act

Products must be as advertised, and you must not give misleading information.

9. Distance Selling Act

Some selling methods, such as online purchasing, require you to provide a “cooling-off” period during which a consumer can cancel a purchase and receive a refund.

10. Develop internal legal documents

Internal legal documents build trust in your company for the benefit of all parties involved, including customers, employees, and potential investors.

11. Privacy policy

A privacy policy informs customers about how their information will be collected, utilised, kept, and protected. It should also specify whether you will share any personal data.

12. Company Handbook

As your business expands, you’ll most likely make changes and additions to your company handbook. In a nutshell, it’s a book that summarises how you run your firm.

It should always be accessible to all employees; you may give everyone a copy or make it easily accessible for reference. Here’s what to include.

- Your company mission statement

- Your company’s policies

- Human resources and legal data related to employment

Final thoughts

Several initiatives specialising in various areas, such as finances, taxation, and business planning, can help and support your UK company.

The cost of launching a business in the UK varies depending on a variety of circumstances. However, several resources are available in the form of UK business grants and loans.

Also, the essential part of setting up a business in the UK is getting started as soon as you’re ready.

As a new business owner, you’ll undoubtedly make mistakes, which is okay – take your time to prepare before taking that first step into the business world. If you’re unsure about something, seek legal or financial advice from a professional.